Women and banking: 50 years of progress

March is Women’s History Month, when we commemorate the ways women have played a vital role in history through their leadership and achievements.

The many areas in which women have made strides during the past five decades include personal finance and banking. Today, more than half of all women are in the workforce, and women can’t legally be denied credit based on gender. However, in 1970, only 43 percent of women were in the labor force, and women could be turned away by lenders if they didn’t have a male co-signer.

Many events over the past half-century have helped to expand the financial rights of U.S. women. Here are several of these milestones through the decades, along with some expert advice for women on personal finance.

Key women in finance statistics

- Among full-time workers, women earn just 83 cents for every dollar earned by men.

- Among parents with children under five, nearly 20 percent of mothers since the peak of the pandemic cite childcare problems as the main reason for not seeking work, compared with less than 5 percent of fathers.

- In 2024, only 7 percent of C-suite positions were held by women of color, compared to 56 percent that were held by white men.

- Twenty percent of women had no emergency savings in 2024, as compared with 14 percent of men.

Sources: Institute for Women’s Policy Research, Pew Research Center, McKinsey & Company, Bankrate’s emergency savings report, U.S. Census Bureau

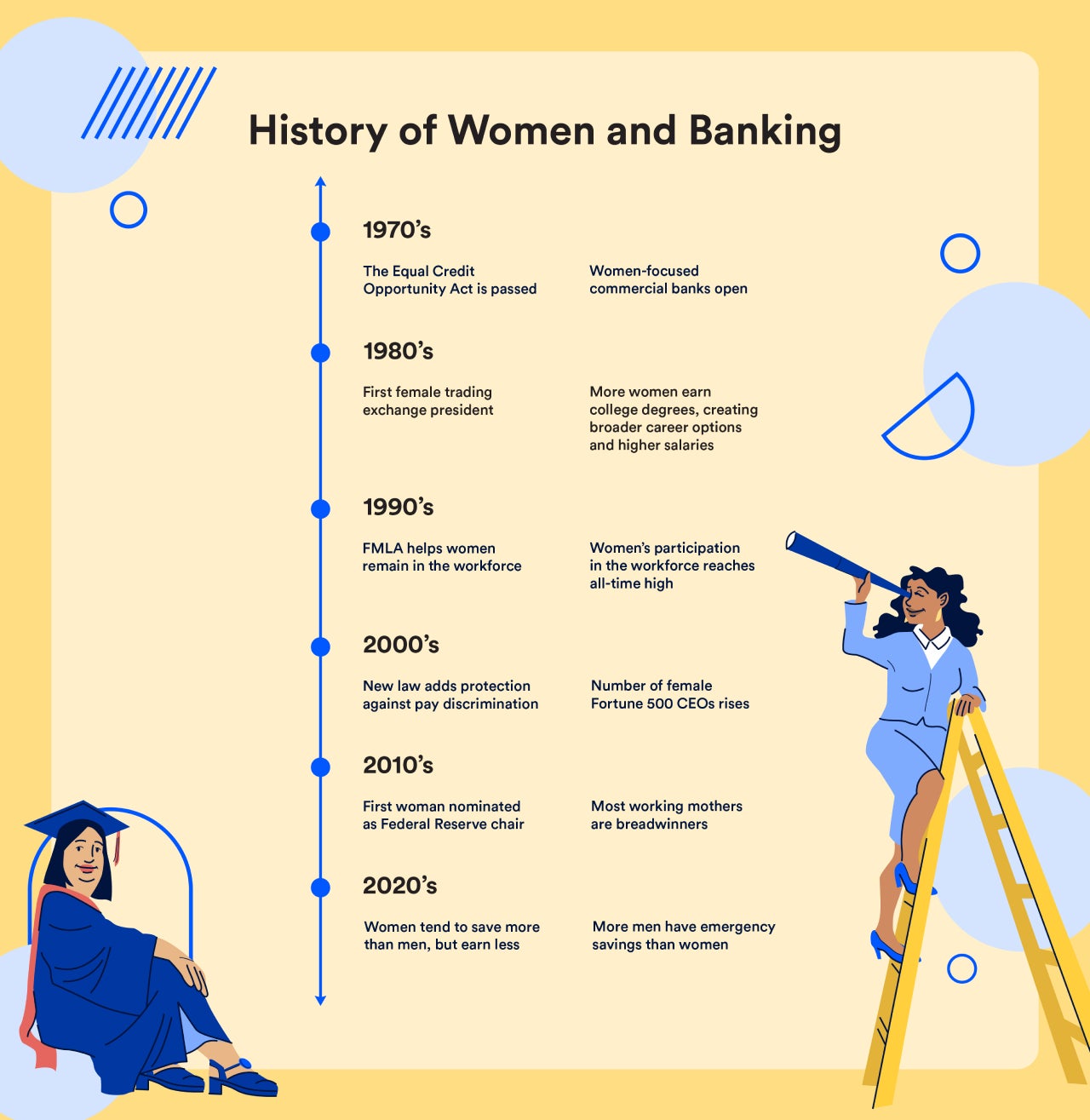

1970s

- The Equal Credit Opportunity Act is passed

- Women-focused commercial banks open

Equal Credit Opportunity Act

Up until the early 1970s, a woman’s application for credit could be denied if a husband didn’t co-sign, which often created obstacles for both married and single women. The Equal Credit Opportunity Act of 1974 changed this by prohibiting credit discrimination based on sex or marital status. The scope of the law was later broadened to protect people based on age, marital status, race, national origin or religion.

Those required to abide by the Equal Credit Opportunity Act include banks, credit unions, department stores and other lenders. This federal civil rights law made a “tremendous difference,” says Mike Sullivan, a personal finance consultant with financial education nonprofit Take Charge America.

Prior to the law, for car loans or financial transactions, a woman was expected to have someone — a father or husband, typically a male — co-sign for that transaction.

— Mike Sullivanpersonal finance consultant with financial education nonprofit Take Charge America

First Women’s Bank

In 1975, First Women’s Bank opened in New York City to cater to women customers and help foster equal opportunities for women in banking. Women’s rights activist and writer Betty Friedan was an organizer and director of the full-service bank, which also provided educational services for women. A handful of other women-focused banks opened around the same time throughout the country.

While women-focused and women-run banks have been few and far between, First Women’s Bank wasn’t the first of its kind, as a small number of U.S. banks made it a priority in the 19th and 20th centuries to help women utilize their products and services.

Another women-focused financial institution that opened in the 1970s was the Detroit Feminist Federal Credit Union, which was based in Detroit and set out to provide services such as loans and financial education to women who’d faced discrimination in the traditional lending market.

Other similar credit unions were subsequently launched in places like Maryland and Washington, D.C. They also aimed to provide financial products and services to women who’d been denied them elsewhere.

1980s

- First female trading exchange president

- More women earn college degrees, creating broader career options and higher salaries

Rosemary McFadden heads the NYMEX

Women broke ground by taking on high positions in financial institutions toward the end of the 20th century. Rosemary McFadden became the first female president of the New York Mercantile Exchange (NYMEX) in 1984, making her the first woman to head any trading exchange in the United States.

As NYMEX president, McFadden was paid a six-figure salary, and her job was to oversee the daily operations of the exchange and make policy recommendations. By the time she left in 1989, the exchange’s volume of contracts had expanded to 34 million from 5 million.

Education and career opportunities

The 1980s was a time when U.S. women earned college degrees in increasing numbers, securing slightly more than half of bachelor’s degrees awarded during the decade. Women also were awarded about half of the master’s degrees and roughly one-third of the doctorates given during this time.

Obtaining college degrees afforded women access to careers that had previously been unavailable to them, which also led to increased earnings, helping to narrow the income gap significantly over a decade. In 1979, women earned just 62.3 cents for every dollar men did, but by 1989, women’s pay increased to 70.1 cents for every dollar men earned, according to the U.S Bureau of Labor Statistics.

Today, women have gained some ground when it comes to taking on higher positions in the workplace and earning college degrees, yet they make up less than half of senior leadership roles in the workforce.

Key present-day women’s education and career statistics

- Women now account for more than half (50.7 percent) of the college-educated workforce.

- Women hold only 35 percent of senior leadership positions in today’s professional world.

- Only slightly more than 10 percent of Fortune 500 CEOs are women.

- Women earn a median of 83 cents for every dollar earned by men.

Sources: Pew Research Center, Zippia, Women Business Collaborative, Bureau of Labor Statistics

1990s

- FMLA helps women remain in the workforce

- Women’s participation in the workforce reaches all-time high

Family and Medical Leave Act

Soon after women made strides in education and the workforce in the 1980s, a groundbreaking law took effect that would help many keep their careers on track. The Family and Medical Leave Act (FMLA), passed in 1993, enables covered employees to receive up to 12 weeks of unpaid time off for events like childbirth and newborn care, as well as caring for a spouse, parent or child with a serious health condition.

Today, around 15 million workers each year take FMLA-related leaves, and FMLA has been used more than 500 million times in total. The majority (92 percent) of employers report no difficulty complying with FMLA.

The most common reasons workers take FMLA leave include:

- Tending to their own health conditions (52 percent)

- Caring for a newborn, an adopted child or a foster child (21 percent)

- Caring for a spouse or parent (17 percent)

High workforce participation, big gender pay gap

The passing of FMLA made it easier for women to remain in the workforce after having children, and by 1996, 60 percent of married couples had income from both partners, compared with just 44 percent in 1967. By the early 2000s, labor force participation by women peaked at 60.3 percent, and has remained slightly lower ever since.

Though record numbers of American women held jobs in the 1990s, the gender income gap was still prevalent by the end of the decade: Median earnings for men and women in 1999 were $61,402 and $44,402, respectively.

2000s

- New law adds protection against pay discrimination

- Number of female Fortune 500 CEOs rises

Lilly Ledbetter Fair Pay Act

In 2009, a federal law was passed that strengthened protections for workers like women and other minorities against pay discrimination. Named the Lilly Ledbetter Fair Pay Act and signed by President Barack Obama, the law established that liability may “accrue” whenever a paycheck is received that is deemed discriminatory based on sex, race, color, religion or national origin.

By stating that wage discrimination claims can be filed up to 180 days after the last discriminatory paycheck was issued, the law increases the ability of employees to file claims in cases where they were not yet aware of discrimination when it occurred.

Workers who feel they’ve been discriminated against and wish to seek recourse can do so by filing a charge with the U.S. Equal Employment Opportunity Commission, a federal agency tasked with enforcing anti-discrimination laws in the workplace. Once a charge is filed, the agency assesses the allegations and makes a finding, after which it may attempt to settle the charge or file a lawsuit.

2010s

- First woman nominated as Federal Reserve chair

- Most working mothers are breadwinners

Janet Yellen heads the Fed

In addition to holding more senior positions in corporate America, women have made history in recent years by taking the helm of some government financial institutions. Economist and educator Janet Yellen became the first woman to lead the century-old Federal Reserve in 2014. Part of Yellen’s role during her single four-year term was to keep the country’s economic recovery on track after the Great Recession. (Yellen later went on to join President Joe Biden’s cabinet in 2021 as the first female Secretary of the Treasury.)

Low interest rates were maintained during Yellen’s time as chair of the Fed, which was also a time of job and wage growth. Yellen initiated a reversal of some policies that were in place as a result of the 2008 subprime mortgage crisis. One program she oversaw involved selling mortgage and Treasury bonds the Fed had purchased to help stimulate the economy.

Increase in breadwinning moms

Data shows that families have been increasingly dependent on women’s earnings to survive. In the years leading up to the COVID-19 pandemic, two-thirds of women were either the sole breadwinner or a co-breadwinner for their households, according to the Center for American Progress. The 2019 study also found:

- Three-quarters of mothers of older children (ages 6 to 17) were in the labor force.

- Two-thirds of mothers of younger kids (under age 6) held jobs.

- Utah was the state with the lowest rate of breadwinning moms (1 in 4).

- The District of Columbia had the highest rate, with slightly more than half.

Present day

- Women tend to save more than men, but earn less

- More men have emergency savings than women

- Women-owned banks are few and far between

Earnings vs. savings

In addition to the persistent gender pay gap, women have some ground to gain regarding increasing savings and having an adequate emergency fund.

When it comes to saving money, women put away a slightly higher percentage of what they earn than men. According to a Fidelity study, women save an average of 9 percent of what they earn each year, while men save 8.6 percent.

A higher savings rate doesn’t necessarily translate to women having more money in the bank than men, however, since women continue to earn less than men. While the gender pay gap has been gradually decreasing over the decades, women earned a median of 83 cents for every dollar men earned in 2024, according to the Bureau of Labor Statistics.

Men are in better shape than women when it comes to having money saved for emergencies, with women more likely than men to say they had no emergency savings in 2024 (20 percent vs. 14 percent).

Data shows men are also slightly more likely than women to be fully banked, meaning they had a checking account or high-yield savings account at a federally backed bank or credit union and didn’t rely on a payday loan or other alternative financial services.

In the Federal Reserve Board’s 2020 Survey of Household Economics and Decisionmaking, 15 percent of men reported having relied on such alternative financial services within the previous year, compared to 17 percent of women.

Women-owned banks

In 2021, the U.S. Federal Reserve announced it would begin including women-owned financial institutions under the umbrella of minority depository institutions (MDIs). Today, only 18 women-owned banks are listed as MDIs by the Office of the Comptroller of the Currency.

One bank that opened in recent years with a goal of helping women entrepreneurs generate capital is First Women’s Bank. Established in 2021, the Chicago-based bank offers deposit products as well as small business administration and commercial loans. The bank’s website bills itself as “the nation’s only bank with a strategic focus on supporting the women’s economy and closing the gender lending gap.”

Examples of other woman-owned banks include Beacon Business Bank in San Francisco, First National Bank in Tigerton, Wis., and The Santa Anna National Bank in Santa Anna, Texas.

Bottom line

During the past 50 years, women have made strides in gaining access to credit, investing, higher education and more career opportunities. Further diversity, awareness and education can help to even the playing field for women and other minority groups when it comes to banking and personal finance.

“The banking sector and financial services, generally, are still very male dominated,” says Cady North, CEO of North Financial Advisors. “All banks would be able to better serve women customers if their teams were more gender and ethnically diverse.”

Why we ask for feedback Your feedback helps us improve our content and services. It takes less than a minute to complete.

Your responses are anonymous and will only be used for improving our website.